Bulkhead τ · RVH Track

Rough Volatility as ML Benchmark

Two papers on why domain expertise — not ML capability — is the binding constraint

in rough volatility forecasting and semiconductor yield prediction. The naive pipeline

fails structurally at every layer. The failures are predictable, diagnosable, and

invisible to a practitioner who does not know the process.

The two papers

Design Principle and Concrete Domain

Paper 1.8 — Cross-Domain Benchmark Principle

Rough volatility as a reusable benchmark design criterion

Both realized volatility forecasting (empirical, H ≈ 0.1) and semiconductor

defectivity simulation (H = 0.1 by design) reward domain expertise at every

pipeline layer. Partial corrections produce plausible-looking but still

systematically wrong results — making shallow domain expertise detectable.

The 7.1% instability loss in the fab simulation is visible only through path

modeling; the static average erases it.

Four conditions. Two domains. One benchmark design principle.

Paper 1.9 — Concrete ML Evaluation Domain

Realized volatility forecasting as the financial benchmark

The generative process — fractional Brownian motion, H ≈ 0.1, validated across

thousands of assets — is structurally incompatible with every standard ML

architecture. LSTMs, Transformers, and AR models carry Markovian inductive

biases that conflict with rough volatility. The mismatch is not tunable; it is

architectural. HAR-RV is the expert floor, not the ceiling. An evaluator's job

is to determine whether a practitioner knows to start there — and why.

Know the process before fitting any model. That is the bar.

What rough volatility is

H ≈ 0.1 — Rougher Than Brownian Motion

The Process

Fractional Brownian Motion

Realized volatility behaves like a fractional Brownian motion with Hurst

exponent H ≈ 0.1 — empirically validated across thousands of assets by

Gatheral, Jaisson, and Rosenbaum (2018). H < 0.5 means anti-persistent

increments: positive moves are more likely to reverse than continue.

At H = 0.1 the paths are substantially rougher than standard diffusions.

The Consequence

Clustering and Anti-Persistence Together

Volatility clusters at high levels — when it rains, it pours — while

increments remain anti-persistent. This two-layer structure is what makes

finite-context architectures structurally misspecified.

Adding depth or attention heads does not fix a Markovian bias.

Four pipeline layers

Where The Naive ML Pipeline Fails

Layer 1

Feature Engineering

Default (wrong): raw daily returns.

Domain-correct: log-realized variance at 5-minute, 1-hour, and daily frequencies plus bipower variation.

Raw daily returns have near-zero autocorrelation — the signal has already decayed.

A model ingesting raw returns is fitting noise. This is not a hyperparameter

problem; it requires knowing what the relevant process signal is.

Layer 2

Architecture Selection

Default (wrong): LSTM, Transformer, AR.

Domain-correct: HAR-RV, rough fractional kernel, neural-SDE.

Standard architectures carry Markovian inductive biases that cannot represent

fBm long-memory structure. The mismatch is architectural, not a scale problem.

Deeper LSTMs do not resolve it.

Layer 3

Validation Protocol

Default (wrong): k-fold cross-validation.

Domain-correct: expanding-window walk-forward with 252-day burn-in.

K-fold on a long-memory series allows future path information to contaminate

training. In-sample metrics look strong; out-of-sample performance collapses

during volatility regime shifts — exactly when the model is needed most.

Layer 4

Evaluation Metric

Default (wrong): MSE.

Domain-correct: QLIKE.

MSE over-penalizes large absolute errors without normalizing by the current

volatility level. QLIKE weights proportional errors and is the standard

criterion for volatility model comparison (Patton, 2011). A model optimized

on MSE is systematically miscalibrated during high-volatility regimes.

The interaction structure

Corrections Are Jointly Necessary

Three out of four is not enough

Wrong features mask architecture failure in-sample — the model overfits noise

with sufficient capacity. Wrong validation masks both. Wrong loss hides

miscalibration until an out-of-sample volatility spike. A practitioner who

corrects any three but not the fourth still produces a systematically

miscalibrated result.

Shallow knowledge is detectable

A practitioner who knows two of the four corrections will be confidently wrong

in specific, diagnosable ways that a domain expert can predict before seeing

the model output. This is what makes the domain high-signal benchmark territory:

partial expertise produces confident wrong answers, not noisier correct ones.

The expert floor

HAR-RV Is Not A Simplification

Model

HAR-RV (Corsi, 2009)

A linear heterogeneous autoregression on daily, weekly, and monthly realized

variance components. No hidden layers. No attention. Interpretable: each

coefficient maps directly to the multi-scale persistence structure of the

process. Hard to beat at standard evaluation horizons.

Why It Matters

It Is A Statement About The Process

HAR-RV encodes the heterogeneous structure of rough volatility directly.

A practitioner who knows this domain knows to start here. A practitioner

who does not will likely never produce HAR-RV through search — the standard

ML instinct is to add complexity, not to remove it.

Empirical evidence — Paper 1.9

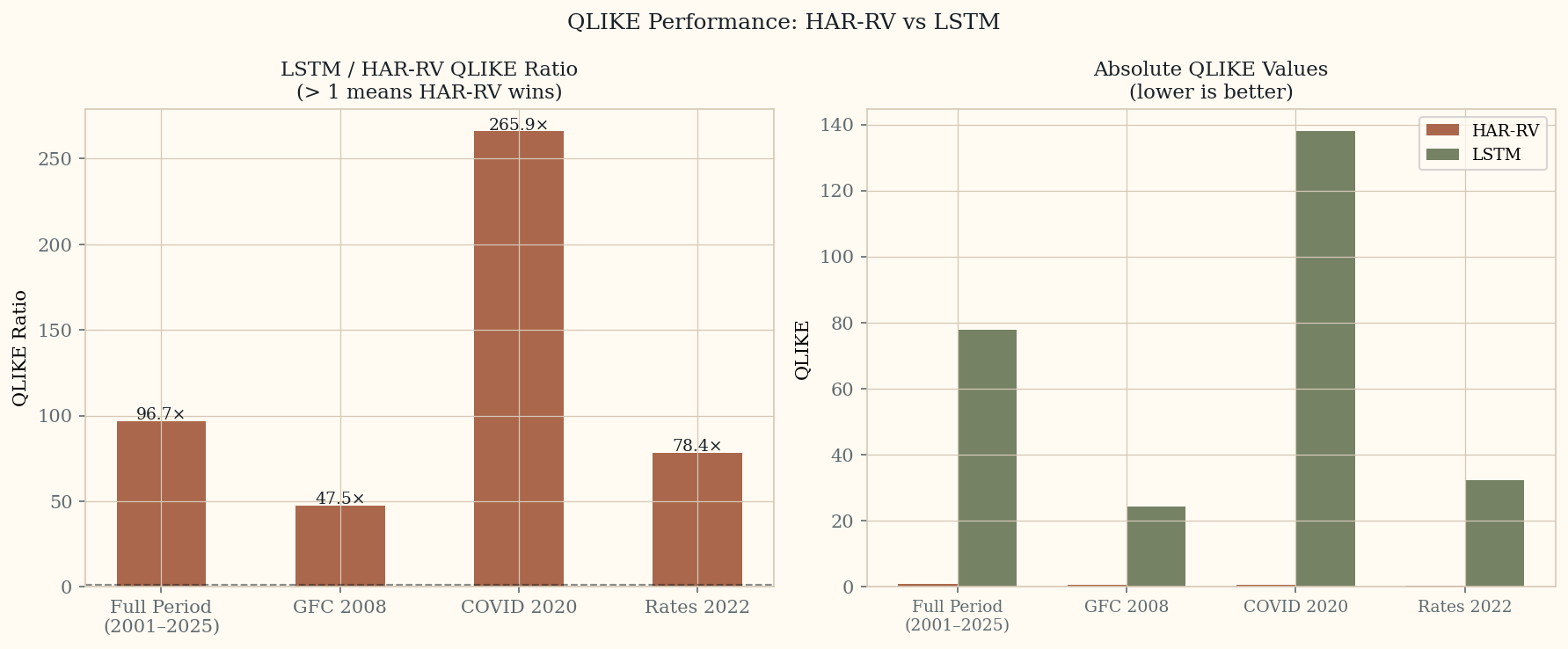

HAR-RV vs LSTM: Walk-Forward Results (S&P 500, 2001–2025)

Walk-forward validation on 6,264 out-of-sample predictions. Expanding window,

252-day burn-in. HAR-RV uses OLS on daily, weekly, and monthly realized variance

components. LSTM trained on the same features with MSE loss — intentionally the

wrong loss function, as the paper describes.

Full Period QLIKE Ratio

96.7×

LSTM / HAR-RV over 2001–2025. HAR-RV wins across all 6,264 predictions.

COVID 2020 QLIKE Ratio

265.9×

LSTM degrades worst precisely during the highest-stress period — when the model is needed most.

Left: LSTM/HAR-RV QLIKE ratio by period — values above 1 mean HAR-RV wins.

Right: absolute QLIKE values — HAR-RV stays near zero across all periods while LSTM spikes at every stress event.

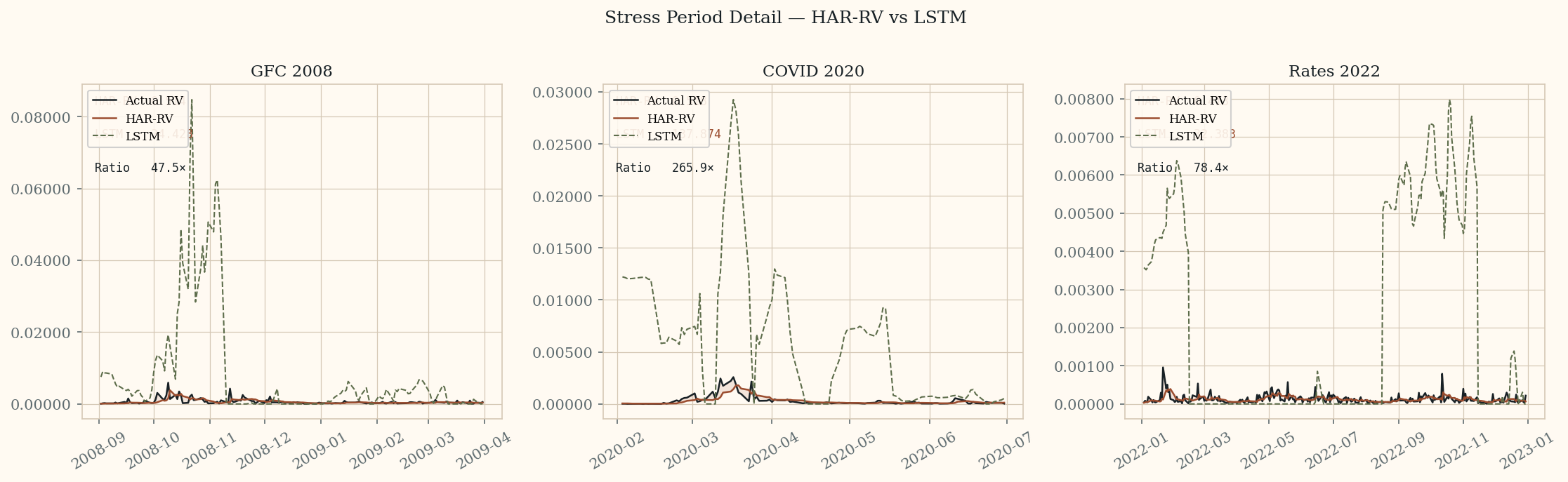

Stress period detail. HAR-RV (red) tracks actual RV (black) closely in all three periods.

LSTM (green dashed) overshoots dramatically — particularly during COVID 2020 where it reaches

137.87 QLIKE vs HAR-RV's 0.518.

Cross-domain comparison

Two Domains, One Benchmark Property

Financial (empirical)

fBm, H ≈ 0.1, validated across thousands of assets. Default pipeline misses clustering through Markovian bias.

Semiconductor (modelled)

fBm, H = 0.1, design choice. Static D₀ average erases 7.1% instability loss visible only through path modeling.

Shared Failure

Naive pipeline produces plausible in-sample results that miss operationally significant behavior at regime shifts.

Shared Correction

Domain-informed structure owns the modeling correctness. The ML pipeline sits on top of it — it does not replace it.

Expert Bar

Know which pipeline choices are wrong for this process — and why — before fitting any model.

Four benchmark conditions

What Makes A Domain High-Signal For Testing Expertise

Condition 1

Structural Failures

Pipeline failures are correctable only by changing the modeling approach — not by tuning hyperparameters.

Condition 2

Process Knowledge Required

The correct approach at each layer requires understanding the process, not just fitting the data.

Condition 3

Pre-Fit Diagnosability

A domain expert can identify which pipeline choices are mismatched before fitting any model.

Condition 4

Partial Knowledge Is Detectable

Partial corrections produce plausible-looking but still systematically wrong results. Shallow domain expertise is visible.

One-line thesis

What These Papers Are Actually Saying

Domain expertise is testable. A practitioner who knows rough volatility can specify

the correct pipeline before seeing the data — because they understand the process.

One who does not will be confidently wrong in ways a domain expert can predict in advance.

Related work

Companion Site

The semiconductor simulation that motivated the cross-domain principle is documented at

Fab Simulation & RVH — Paper 1.4.